Why Wealthy Clients Borrow

According to Tesla's 2023 proxy statement, Elon Musk has pledged 238,441,261 shares of Tesla (valued at $57.9B as of August 11th, 2023) to secure personal indebtedness. The wealthiest person in the world uses over a quarter of his net worth as collateral for loans. Why? Why would any wealthy person borrow at all? In nearly two decades of underwriting and structuring billions of dollars of loans for wealthy individuals, this is the most common question from family, friends, and acquaintances.

While the nuances of each client's financial situation are private and varied, a few common threads drive a wealthy individual or family's decision to borrow. First, all wealth isn't liquidity. Until we establish a barter system, you cannot exchange a Rembrandt or a share of Apple for groceries or to pay off a tax liability, and even then, you may not want to. Second, cash flow isn't wealth. Varying tax rates, liabilities, saving habits, and living expenses make it nearly impossible to assign real value to cash flow or income in a silo. Third, all balance sheets are not created equal. Some billionaires have extremely diversified and liquid balance sheets. Others have balance sheets made up almost entirely of single illiquid positions. In the volatility over the last few years, many billionaires tragically lost their third comma. Some lost two.

Because of the idiosyncrasies of every situation, the question of why a wealthy person may (or perhaps should) borrow can be a lot more complicated than you'd suspect. We'll analyze some more popular reasons in this piece, but this will hardly be exhaustive. Contact us to walk through how our platform, Sandbox Record, can help you manage your entire balance sheet or how we can help deliver the liquidity solution that's right for you.

Global wealth is, in fact, mostly illiquid. According to Boston Consulting Group's 2023 Global Wealth Report, financial wealth declined in 2022 by 4% to $255T, a slight decline relative to the 10% jump experienced in 2021. Compare this drop to the 5.5% increase in the value of tangible assets, including real estate, rare wines, and fine art. These assets are now worth a staggering $261T.

BCG projects that the delta between tangible and financial assets will diverge further. They estimate that illiquid assets will be valued at $341.2T in 2027 compared to $329.1T for financial assets.

A survey performed by Goldman Sachs supports BCG's thesis. In their One Goldman Sachs Family Office initiative, "35% of respondents indicated that they plan to reduce their allocation to cash and cash equivalents in the next 12 months."

So, where is all this cash coming from? The respondents to Goldman's survey only hold 12% of their assets in cash. 41% plan to increase their allocation to private equity. 30% plan to increase their allocation to private credit. Our thesis is that many participants in the private markets will borrow to fund these investments, and given the shift to tangible assets, these are the assets that may best serve as collateral for these loans. Because of the risk of lending against these assets, however, lenders will reserve these facilities for those who thread the needle between substantial illiquid assets but sufficient liquidity and cash flow to service and eventually repay the debt.

How do our partner firms figure into this equation? Unsurprisingly, the trend in the direction of tangible assets (and away from financial assets) has impaired the profitability of wealth managers. Per BCG, Assets Under Management declined by 10.5% in 2022, driven primarily by poor market performance. In North America, this drop in AUM increased the importance of the banking portfolio, primarily in lending, as loans grew by 15% as a share of the business mix reported by wealth managers.

It would seemingly benefit wealth managers to look to banking (particularly lending) to offset the projected declines in liquidity held by wealthy families.

Quickly browse any list of the wealthiest people in the world, and you'll find some similarities. The current top 10 (according to Bloomberg) earned their wealth by leading large, publicly traded companies. Most were founders.

Despite this, and the proliferation of HENRYs (High Earners, Not Rich Yet), many still associate wealth with income. But browse the Tesla proxy a bit further, and you'll notice that Mr. Musk has never accepted a salary from Tesla. Mark Zuckerberg and Larry Ellison earn an annual salary of $1. Bill Gates resigned as Chairman of Microsoft nearly a decade ago.

For many U/HNW individuals, W2 income may be insignificant or non-existent. Cash flow may come in various forms, including Schedule C, distributions, interest, and dividends. This income may be predictable, but very often, it isn't, potentially leaving individuals and families unprepared for liquidity needs.

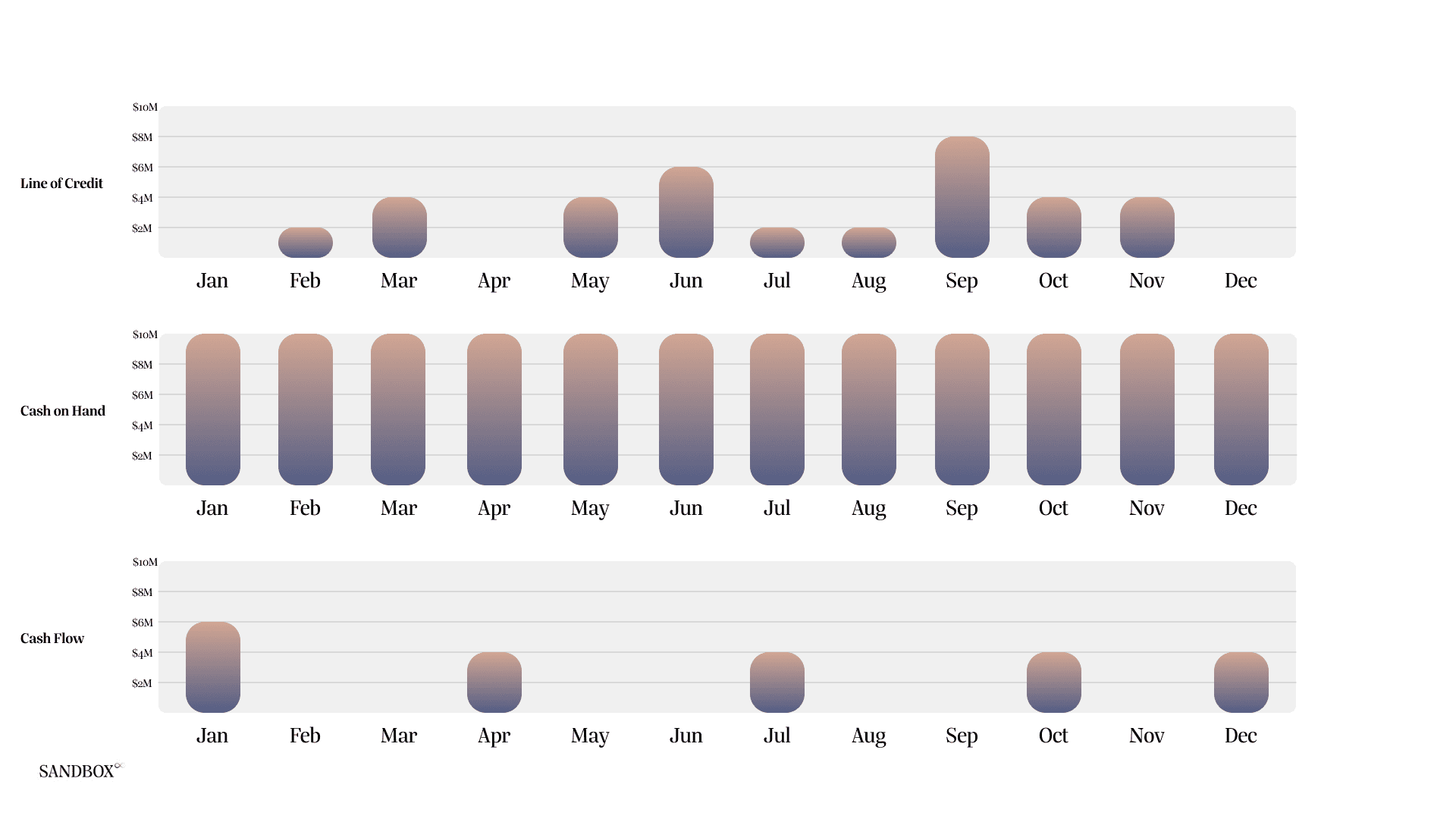

Wealthy clients often use credit facilities to fill those gaps in cash flow. Let's say a family has $100M in assets, and they'd like to maintain 10% in cash over the course of a year, but would also like to take advantage of opportunistic investments, make quarterly tax payments, or acquire a property abroad. They receive distributions from a variety of sources periodically, including an annual distribution in December from a trust, and quarterly payments from a closely held business. In the simplified charts below, you can see that the client is able to maintain their desired 10% allocation to cash, use a revolving credit facility to fund general expenses and private investments, then use their periodic cash flow to pay down the loan.

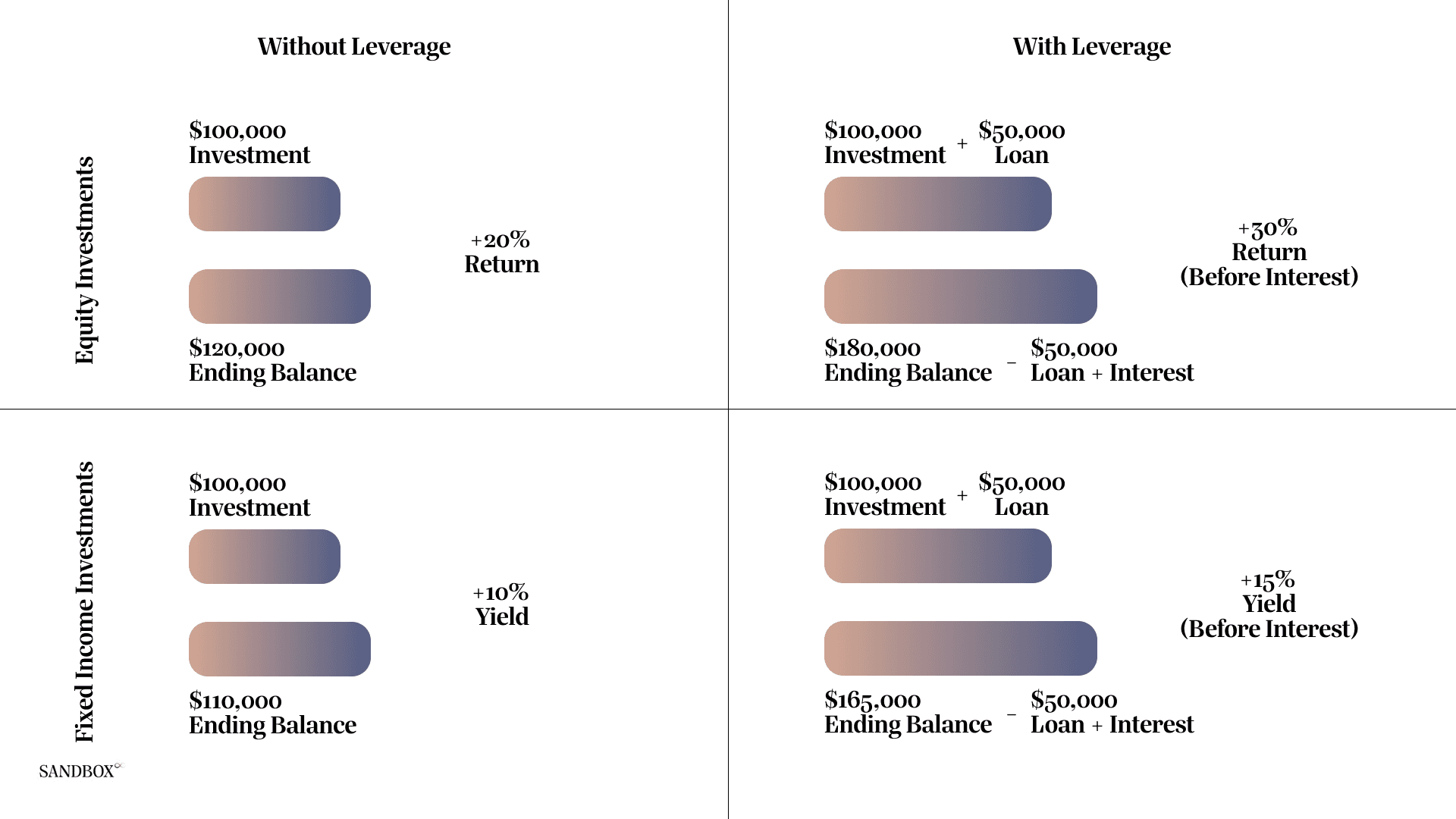

A levered investment can span the entire risk spectrum. Many consider the most common levered investment, a residential mortgage, a necessary step of the home buying process. Most retail and mass affluent borrowers acquire more than they can afford if forced to pay cash. Nearly all would be locked out of the housing market without access to mortgages. Amazingly, over the last 60 years, no financial product has been more responsible for creating wealth than the 30-year mortgage. Simply put, this is because while you acquire an entire home, you only pay for a small percentage upfront. A mortgage allows you to participate in theoretically unlimited upside, with your downside limited to the cost of the home plus interest.

Unlimited upside sounds great, in theory, but during periods of volatility, this bet can leave homeowners owing more than their home is worth. There was a flood of instances like this in 2008, and the entire economy suffered, leading to several bank failures, forced mergers, and substantial government intervention to prevent a second depression.

While many wealthy clients could pay for their residence multiple times over without a mortgage, they often use their mortgage to express a view on interest rates and the housing market. Bulls would naturally want to use more leverage to maximize the return on their equity. Bears would borrow less to reduce the risk of their loan being underwater.

HNW clients often use leverage in the public markets as well. These loans are mostly in the form of margin facilities, where diversified pools of collateral are used to secure loans to invest in additional assets. Additionally, certain derivative instruments (e.g., Total Return Swaps), which made headlines in 2021, where a client can gain access to high-octane leverage in the OTC markets. The collapse of Archegos Capital Management, where Credit Suisse famously lost $5.5B, was the result of outsized, one-way bets on volatile assets with razor thin margin requirements using this sort of investment. It is possible to use these instruments responsibly, but when used irresponsibly, these positions can quite literally destroy billions of dollars of wealth and a 170 year old institution.

Imagine you are the founder of a company worth hundreds of billions of dollars. You acquired nearly all your stock before the company went public, and it has since appreciated over 100,000%. You have twelve figures of unrealized capital gains. If you sold all of your shares, your capital gains taxes would have a material impact on the national deficit.

In this case, it would likely be worthwhile to consider borrowing. Fortunately, despite all of the talk of a wealth tax recently, the tax code as it stands today encourages you to hold and borrow. This comes with the added benefit of a "step-up" in cost basis upon your passing, which means other than the customary estate taxes, your heirs will not be on the hook for any tax related to unrealized capital gains that had accumulated while you were alive. Tabula rasa.

Of course, there are only so many that fit the description above, but these same strategies can be used by virtually any wealthy individual or family with the means to establish and monitor these solutions.

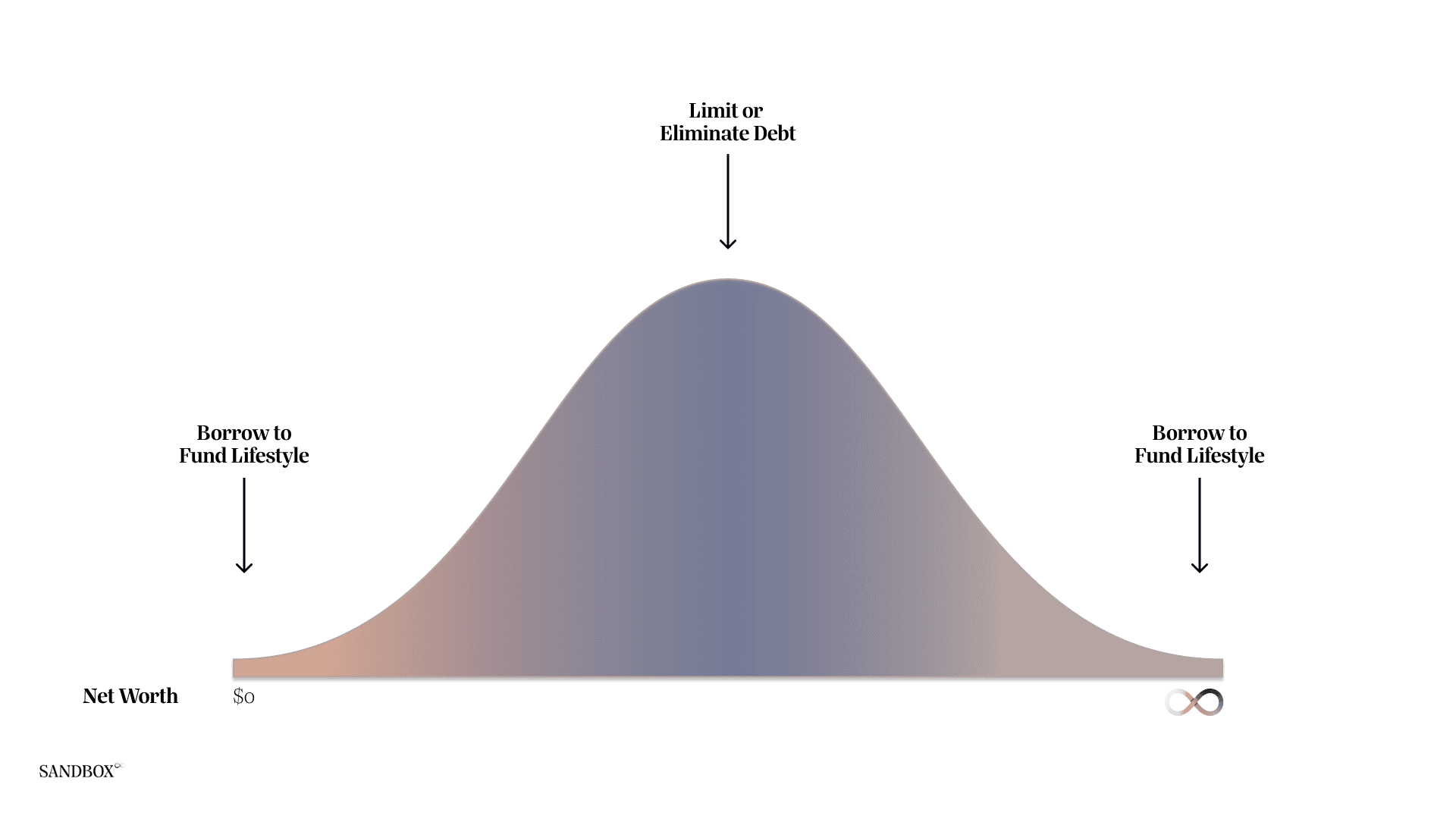

If used responsibly, debt is a tool that can help create capacity on your balance sheet, smooth out cash flows, create tax efficiencies, and augment returns on investments. It is critically important that clients keep a watchful eye on their financials when borrowing, because there are certainly risks that must be addressed if and when they arise. Understanding your current balance sheet, future cash flows, trends, and potential hurdles is essential before putting any material amounts of debt in place. At Sandbox, we're building tools for clients to get up to speed on their current financials quickly and to help them make intelligent, strategic decisions based on tactical data.